The State of AI 2025 - Bessemer Venture Partners

The State of AI 2025

AI benchmarks

Roadmaps for the AI cosmos

2025 predictions

The founder’s edge

The State of AI 2025

Three years after the AI Big Bang early galaxies are forming in the Cloud AI universe, with plenty of “dark matter” still swirling.

In this State of AI report, we aim to:

*Debates continue over the true AI Big Bang—some point to 2012’s AlexNet breakthrough in deep learning; others to OpenAI’s 2020 scaling laws. For this report, we consider the mass release of ChatGPT as the moment AI truly exploded into public consciousness.

AI benchmarks: What “great” startups look like in 2025

Benchmarks have always been an imperfect way to judge startups—but in the AI era, they’re even less reliable. In particular, some AI startups have achieved growth rates the world has truly never seen, driving every AI founder to wonder what good even looks like anymore. We’ve thus updated our benchmarks acknowledging that some AI startups are playing a different game.

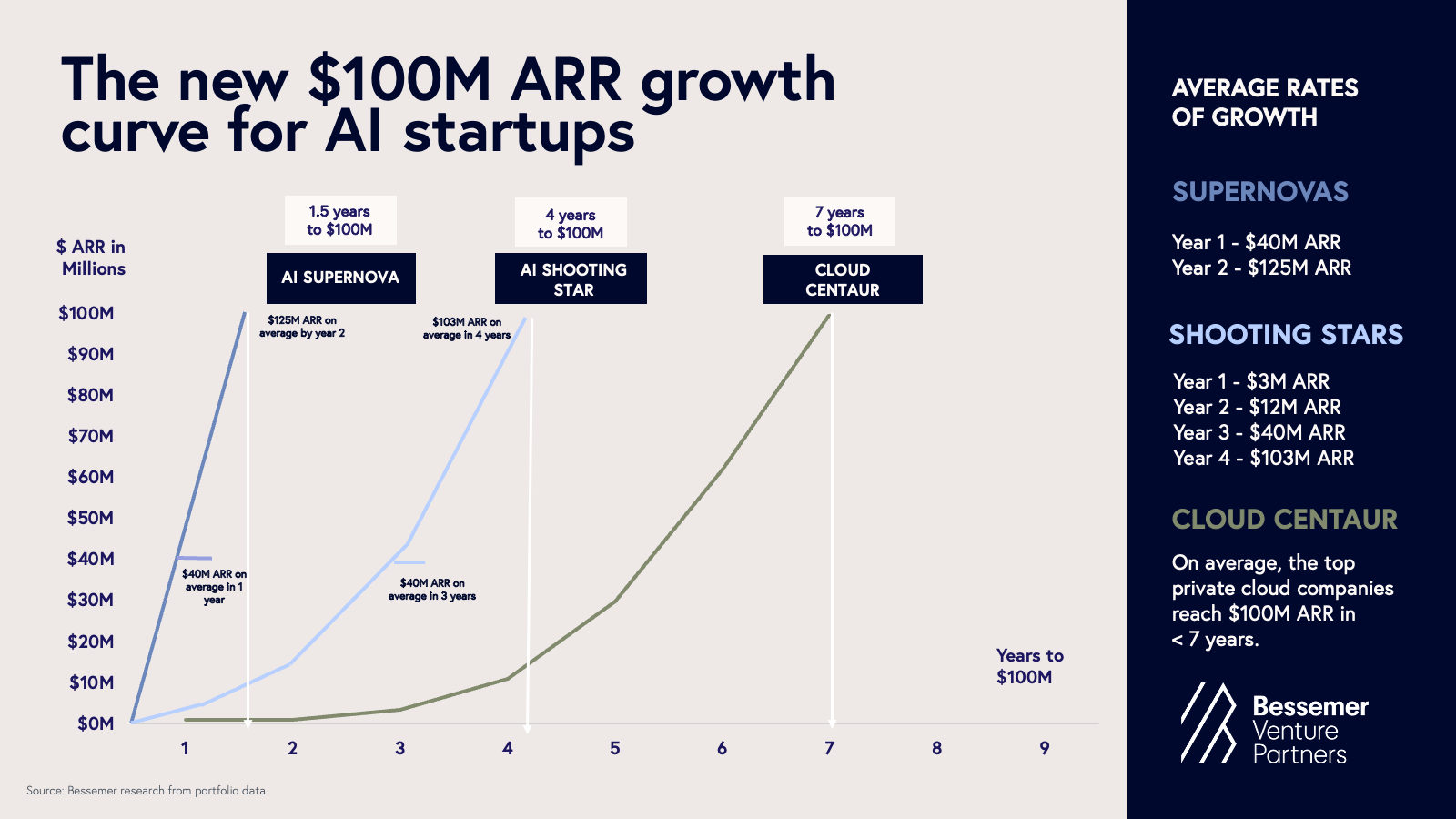

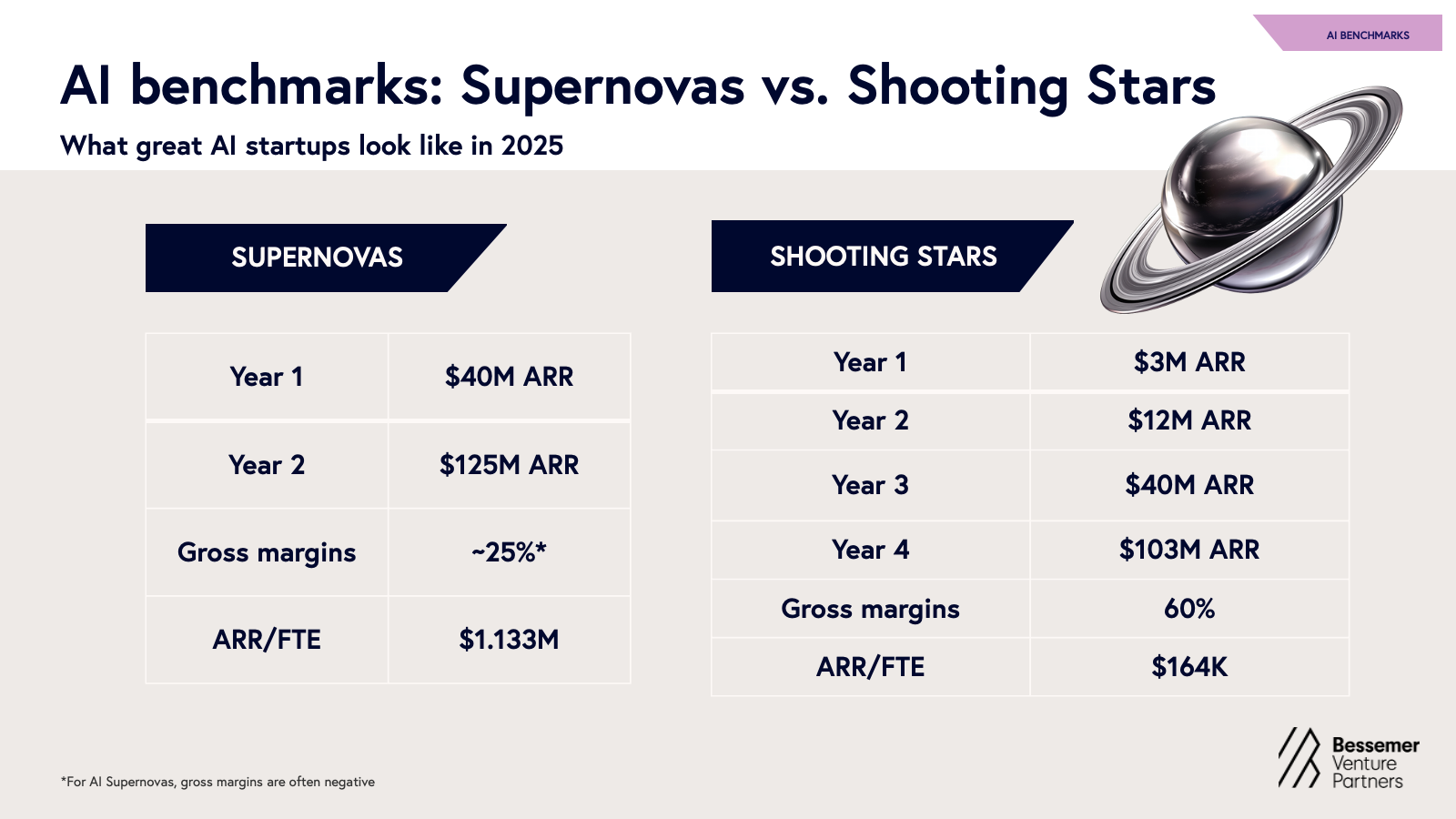

A tale of two AI startups and the new “T2D3”

To formulate our new set of benchmarks we studied 20 high-growth, durable AI startups across our portfolio and beyond, including breakouts Perplexity, Abridge, and Cursor.

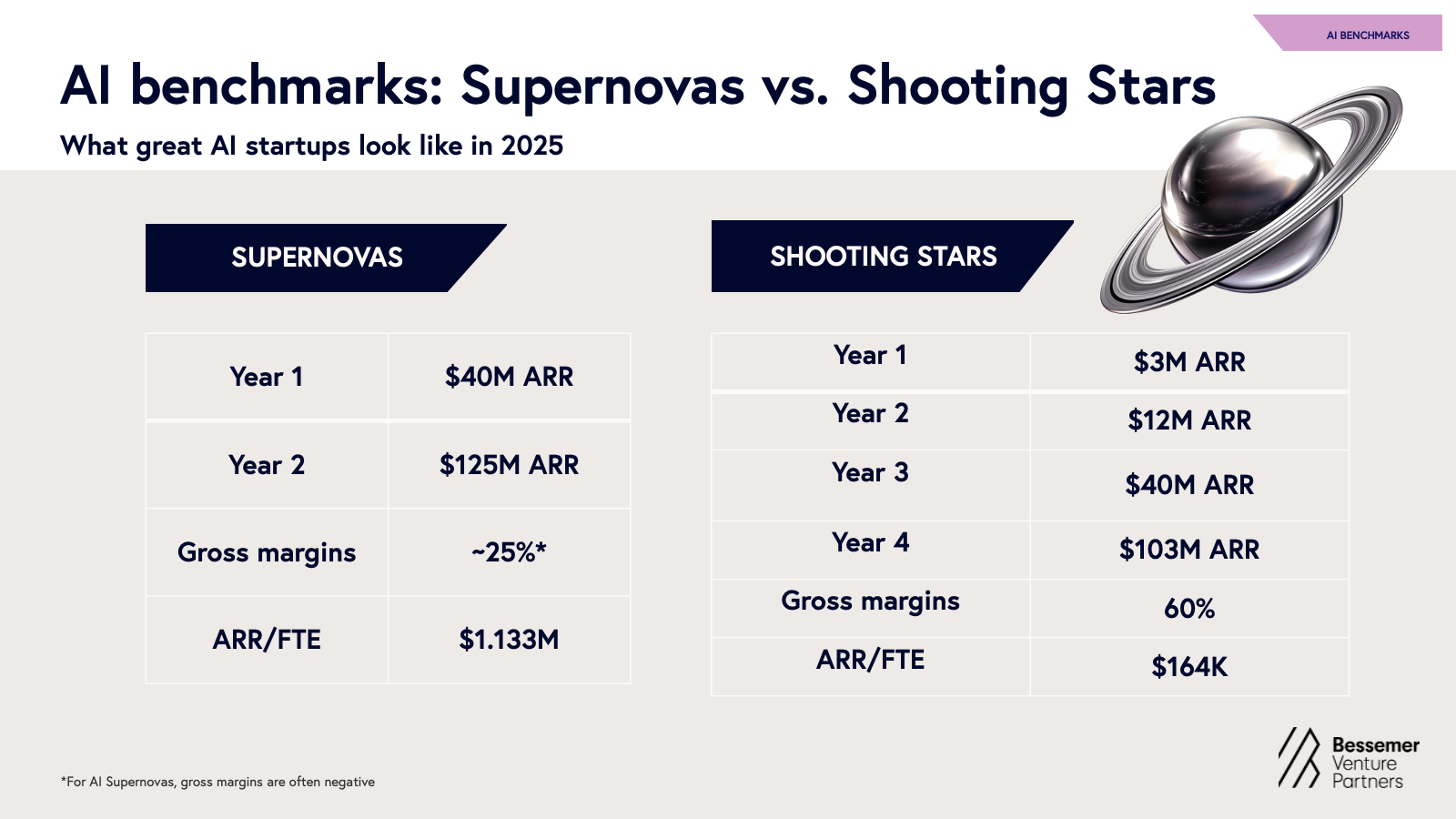

AI supernovas

Supernovas are the AI startups growing as fast as any in software history. These businesses sprint from seed to $100M of ARR in no time, often in their first year of commercialization. These are at once the most exciting and the most terrifying startups we see. Almost by definition, these numbers arise from circumstances where revenue may appear vulnerable. They involve fast adoption that either belies low switching costs, or signals massive novelty that may not align with long-term value. These applications are often so close to the functionality of core foundation models that “thin wrapper” labels could be thrown. And in red hot competitive spaces, margins are often stretched close to zero or even negative as startups use every tool to fight for winner-take-all prizes.

AI Shooting Stars

Shooting Stars, by contrast, look more like stellar SaaS companies: they find product-market fit quickly, retain and expand customer relationships, and maintain strong gross margins—slightly lower than SaaS peers due to faster growth and modest model-related costs. They grow faster on average than their SaaS predecessors, but at rates that still feel anchored to traditional bottlenecks of scaling an organization. These businesses might not yet dominate headlines, but they’re beloved by their customers and are on the trajectory to making software history.

Key takeaway for AI founders on these new benchmarks: We share these admittedly freakish new benchmarks to showcase the reality of standout AI startups of the moment. That said, building an iconic AI company doesn’t require quadrupling overnight. Many of the strongest companies will still take a more deliberate path, shaped by product complexity and competitive dynamics.

However, speed matters more than ever. AI has unlocked faster product development, GTM, and distribution—making “Q2T3” (quadruple, quadruple, triple, triple, triple) an ambitious but increasingly achievable benchmark. Dozens of startups have already proven it’s possible—and we believe you can too!

*Admittedly we haven’t seen five years of data yet, so perhaps in years to come we’ll learn these companies won’t truly triple but Q2 T1 D2 isn’t nearly as catchy.

Roadmaps of the AI cosmos

In every roadmap that Bessemer tracks, we’ve seen many elements of the AI stack meaningfully crystallize in the past year, resulting in the formation of several early galaxies. We will survey those galaxies in each roadmap while noting the many areas of “dark matter” where we’re still guessing what the future holds.

I. AI infrastructure

Galaxies forming: Model layer

Let's start with the obvious: a handful of players such as OpenAI, Anthropic, Gemini, Llama and xAI continue to dominate the foundation model landscape, advancing model performance, while simultaneously exploring vertical integration. It’s clear now that big labs are moving beyond offering just foundation models and tooling for model development—these labs are now rolling out agents for coding, computer use, and MCP integrations. Meanwhile, compute costs continue to drop predictably—driven by software innovations, and end-to-end hardware optimization.

AI infrastructure’s Second Act

AI’s first era has been defined by major algorithmic breakthroughs—backpropagation, convolutional networks, transformers. The field is primarily advanced by algorithmic improvements and scaling methods. Accordingly, infrastructure has mirrored this mindset, fueling the rise of giants in areas such as foundation models, compute capacity, and data annotation.

Dark matter: The bitter lesson of AI

Rich Sutton’s “Bitter Lesson” reminds us that the most effective advances in AI have historically come from harnessing computation and general-purpose learning, rather than relying on handcrafted features or human-designed heuristics. As AI infrastructure enters its next chapter, it remains an open question which techniques will prove most effective or scalable as practitioners seek to embed context, understanding, and domain expertise to ensure real-world utility.

II. Developer platforms and tooling

Galaxies forming: AI engineering an integral part of software development

Beyond the infrastructure stack, AI has clearly transformed software development. Natural language has become the new programming interface with models executing on the instructions. In this paradigm shift, the very principles of software development are changing as prompts are now programs with LLMs as a new type of computer.

Galaxies forming: Model Context Protocol (MCP)

A new layer of infrastructure will have profound implications for AI development—Model Context Protocol (MCP). Introduced by Anthropic in late 2024 and quickly adopted by OpenAI, Google DeepMind, and Microsoft, MCP is becoming the universal specification for agents to access external APIs, tools, and real-time data.

Dark matter: Memory, context and beyond

As AI-native workflows mature, memory is becoming a core product primitive. The ability to remember, adapt, and personalize across time is what elevates tools from useful to indispensable. Great AI systems are expanding past recall and evolving with the user. In 2025, large context windows and retrieval-augmented generation (RAG) have enabled more coherent single-session interactions, but truly persistent, cross-session memory remains an open challenge. While the foundational model companies are working on memory, so too are startups like mem0, Zep, SuperMemory, and LangMem by Langchain.

III. Horizontal and Enterprise AI

Galaxies forming: Systems of Record under pressure

In enterprise software, AI is beginning to expose opportunities for startups to disrupt some of the largest horizontal systems of record (SoR). For decades, SoRs like Salesforce, SAP, Oracle and ServiceNow held firm thanks to their deep product surfaces, implementation complexity, and centrality to business-critical data. The businesses enjoyed some of the strongest moats in software. The switching costs were just too high and very few startups even dared to try and unseat them. Now, those moats are degrading.

With AI’s ability to structure unstructured data and generate code on demand, migrating to a new system is faster, cheaper, and more feasible than ever. Agentic workflows are replacing rote data entry, and the typical implementation projects that required armies of systems integrators and years of work are being accelerated by orders of magnitude.

Galaxies forming: Next generation CRM, HR, and Enterprise Search

The big question: Are AI-native challengers creating net-new categories—or are they finally threatening incumbents? In CRM, early signs of disruption are promising. These AI-native tools aren’t just replacing existing CRMs—they’re offering a new kind of experience altogether. They simultaneously offload a tremendous amount of manual work from sales teams which also provides sales managers with intelligent recommendations for where to spend their time based on auto-synthesized deal signals across all their channels. This is a 10x leap, not a 10% improvement.

Dark matter: Enterprise ERP and the long tail of systems of record (SoR)

Despite all this momentum, some of the biggest enterprise surfaces remain surprisingly under-disrupted:

IV. Vertical AI

Last year, we proposed a bold thesis: Vertical AI has the potential to eclipse even the most successful legacy vertical SaaS markets. Our conviction in that thesis is stronger than ever. Adoption continues to accelerate, particularly for vertical workflows that have long been manual, service-heavy, or seen as resistant to technology. This has reshaped our view of so-called “technophobic” verticals. In reality, the issue was never a lack of willingness to adopt new tools, it was that traditional SaaS failed to solve high-value vertical-specific tasks that were multi-modal or language heavy. Vertical AI is finally meeting these users where they are, with products that feel less like software and more like real leverage.

Galaxies forming: Vertical-specific workflow automation

Multiple industries, and surprisingly many of those considered technophobic in past eras, are showing clear signs of meaningful Vertical AI adoption. For example:

Dark matter: Open questions in Vertical AI

For all the momentum, there are still real unknowns in Vertical AI in three key areas:

V. Consumer AI

As the underlying technology evolves, so do opportunities to tap into new consumer needs. Last year, most consumer usage leaned toward productivity-driven tasks, such as writing, editing and searching, as consumers explored the novelty and utility of AI. But we’re starting to see a shift toward deeper use cases, including therapy, companionship, and self-growth. AI is no longer just a tool for task assistance, it’s poking into more meaningful areas of consumers' lives.

Galaxies forming: AI assistants for everyday tasks and creation

Consumers across age groups are increasingly turning to general-purpose LLMs, particularly ChatGPT and Gemini, for daily or weekly assistance (with an estimated 600M and 400M weekly active users as of March 2025, respectively.) What began as a novelty has become a habit, with these tools now serving hundreds of millions of users each week. Even as a long tail of specialized apps emerges, most consumers continue to rely on these general assistants for a wide range of needs, including research, planning, advice, and conversation.

Over the last year, voice emerged as a powerful modality for how consumers interact with these applications. Unlike legacy assistants like Alexa or Siri, LLM-powered voice AI can handle open-ended questions, facilitate reflection, and support more fluid, conversational exchanges, providing an intuitive, hands-free way to interact with technology. Platforms like Vapi in the Voice AI space are helping power consumers’ abilities to interact with machines in a way that spans language, context, and emotion.

Perhaps one of the most meaningful shifts is in how consumers search for information and interact with the web altogether. In this evolving landscape, Perplexity has emerged as a breakout darling. Its model-agnostic orchestration and blazing-fast UX have made it a go-to for AI-native search. With the launch of Comet, Perplexity’s agentic browser, the company is pushing the frontier further, and it may well become the defining form factor for the next generation of agents that are ambient and proactive.

Beyond its emerging role as a superior assistant, AI is also lowering the barrier to creation turning every consumer into a potential creator. Consumers are building apps with tools like Create.xyz, Bolt, and Lovable, generating music with Suno and Udio, producing multimedia with platforms such as Moonvalley, Runway, and Black Forest Labs, and accelerating ideation and iteration with tools like FLORA, Visual Electric, ComfyUI and Krea. AI is transforming everyday consumers into creators, pushing the boundaries of what we once thought possible.

Galaxies forming: Purpose-built AI assistants

As consumers look to integrate AI more deeply into their daily lives, a wave of consumer applications has emerged to address specific needs. One of the fastest-growing areas is mental health and emotional wellness. While “ChatGPT therapy” continues to gain traction, we’re also seeing the rise of purpose-built tools centered on self-reflection and personal growth. This includes AI journals and mentors like Rosebud and gamified self-care companions like Finch, which help users set personal goals, build healthy habits, and track emotional well-being. Character.AI was an early signal of consumer appetite for emotionally expressive AI, but over the past year, that demand has gone mainstream, with LLM-powered tools increasingly designed to support long-term memory, emotional resilience, and self-development.

Dark matter: Clear unsolved consumer pain points

Some of the most obvious consumer use cases remain underserved not due to lack of demand, but because they still require too much manual action on the user’s part. While early agentic products are emerging, the underlying technology is still maturing.

Bessemer's top AI predictions for 2025

1. The browser will emerge as a dominant interface for agentic AI

As agentic AI evolves, the browser is emerging as a potential environment for autonomous execution—not just a tool for navigation, but a programmable interface to the entire digital world.

2. 2026 will be the year of generative video

2024 marked the mainstream inflection point for generative image models. 2025 saw a similar breakout in voice, driven by improvements in latency, awareness, human-likeness, and customization, coupled with massive cost reductions. 2026 is shaping up to be the year video crosses the chasm. Model quality—across Google’s Veo 3, Kling, OpenAI’s Sora, Moonvalley’s Marey, and emerging open-source stacks—is accelerating. We're nearing a tipping point in controllability, accessibility, and realism, that will make generative video commercially viable at scale.

We also expect the next 12 months to clarify the market structure for generative video:

3. Evals and data lineage will become a critical catalyst for AI product development

One of the biggest unsolved bottlenecks in enterprise AI deployment is evaluation. How is the product, feature, algorithm change “doing”? Do people like it? Is it increasing revenue / conversion / retention? Most every company still struggles to assess whether a model performs reliably in their specific, real-world use cases. Public benchmarks like MMLU, GSM8K, or HumanEval offer coarse-grained signals at best—and often fail to reflect the nuance of real-world workflows, compliance constraints, or decision-critical contexts.

4. A new AI-native social media giant could emerge

Major shifts in consumer technology have historically paved the way for new social giants. PHP enabled Facebook. Mobile cameras made Instagram possible. Advances in mobile video propelled TikTok. It’s hard to imagine that the new capabilities enabled by generative AI won’t lead to a similar breakout.

5. The incumbents strike back as AI M&A heats up

After two years of rapid disruption by AI-native startups, the enterprise giants are striking back—not by rebuilding from scratch, but by acquiring the capabilities they need to catch up. In 2025 and 2026, we expect to see a surge in M&A activity as incumbents move aggressively to buy their way into the AI era.

The founder’s edge in the AI cosmos

We’re no longer at the dawn of AI—we’re deep in its unfolding galaxies. Today’s top startups aren’t just building faster software. They’re designing systems that see, listen, reason, and act—embedding intelligence into the fabric of work and life.

Here are the top takeaways for AI application founders

Recommended Articles

Roadmap: AI systems of action

Part I: The future of AI is vertical

Roadmap: Data 3.0 in the Lakehouse Era

Subscribe to Atlas

Venture insights that matter